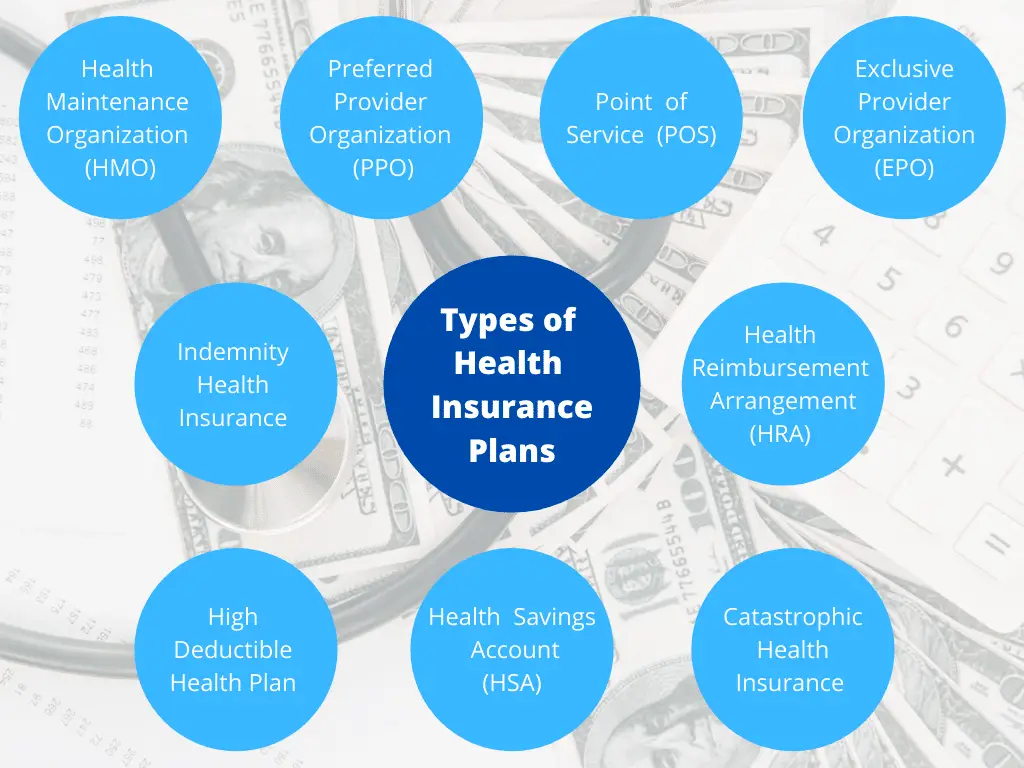

Health insurance can be confusing. There are many types to consider.

Understanding these types helps you make the right choice for your needs. Health insurance is essential. It protects you from high medical costs. But not all health insurance plans are the same. Some cover more than others. Some are expensive, while others are affordable.

Choosing the right type can save you money and ensure you get the care you need. In this blog post, we will explore the various types of health insurance available. This will help you understand their differences and find the best option for you and your family. Let’s dive in and simplify health insurance for you.

Introduction To Health Insurance

Understanding health insurance is crucial in today’s world. Health insurance helps protect you from high medical costs. It provides financial support for medical expenses. Let’s delve deeper into health insurance.

Importance Of Health Insurance

Health insurance is essential for everyone. It ensures you get the medical care you need. Without it, medical bills can be overwhelming. Health insurance covers doctor visits, hospital stays, and medications. It helps you stay healthy without worrying about costs. In emergencies, insurance can save lives. It provides peace of mind knowing you are covered.

Basic Concepts

Health insurance works by pooling risk. Everyone pays a premium. The insurance company uses these premiums to pay for medical costs. There are different types of plans. Some plans have higher premiums but lower out-of-pocket costs. Others have lower premiums but higher costs when you need care. Understanding these concepts helps you choose the right plan.

Deductibles are an important concept. This is the amount you pay before insurance starts covering costs. Copayments are fixed amounts you pay for services. Coinsurance is a percentage of the cost you share with the insurance. Networks are also key. They are the doctors and hospitals that accept your insurance. Staying in-network saves money.

Health insurance can be complex. But understanding these basics can help you make better choices. Choose the plan that best fits your needs and budget.

Individual Health Insurance

Individual health insurance is a policy you buy for yourself. It covers your medical expenses. Unlike group insurance, it is not tied to employment. This type of health insurance provides flexibility and personalized coverage. It is ideal for freelancers, self-employed individuals, or those without employer-provided insurance.

Coverage Details

Individual health insurance offers various coverage options. These include hospital stays, doctor visits, and prescription drugs. Some plans also cover preventive care, maternity, and mental health services. You can choose a plan that fits your health needs and budget. Always read the policy details carefully to understand what is covered.

Pros And Cons

Individual health insurance has several pros. It provides personalized coverage. You can tailor it to your health needs. It is portable. You can keep it even if you change jobs. It offers a variety of plans and coverage levels.

There are some cons too. Premiums can be higher than group insurance. Pre-existing conditions may limit coverage options. Out-of-pocket costs can add up. It is essential to compare plans and understand all costs involved.

Family Health Insurance

Family health insurance is a policy that covers the entire family under one plan. It simplifies managing healthcare expenses by consolidating them into a single policy. This type of insurance is ideal for families looking to protect against unexpected medical costs.

Benefits For Families

Family health insurance offers several advantages. First, it provides comprehensive coverage for all family members. This means medical expenses for parents and children are covered. Second, it usually includes preventive care services. These services help in early detection and treatment of illnesses. Third, having a single policy reduces the hassle of maintaining multiple insurance plans. It is convenient and easier to manage. Fourth, some family health insurance plans offer maternity and newborn care. This is crucial for growing families.

Cost Considerations

Understanding the costs of family health insurance is vital. Premiums are the monthly payments you make for the policy. Deductibles are what you pay out-of-pocket before the insurance kicks in. Co-payments are a fixed amount you pay for specific services, such as doctor visits. Coinsurance is the percentage of costs you share after meeting your deductible. Consider all these factors to understand the true cost of your policy. Some plans may seem cheap but have high out-of-pocket costs. Others might have higher premiums but lower additional costs.

Group Health Insurance

Group health insurance is a type of health coverage offered to a group of people. This kind of insurance is often provided by employers to their employees. The aim is to provide healthcare benefits at a lower cost. This is possible due to the large number of participants.

Employer-provided Plans

Many companies offer health insurance plans to their employees. These plans are known as employer-provided plans. They are designed to cover medical expenses for employees and often their families too. These plans can include a variety of benefits. For instance, doctor visits, hospital stays, and prescription medications.

Employers usually negotiate with insurance companies to get the best rates. This means employees can get more affordable coverage than if they bought insurance on their own. The plans may also offer extra benefits. For example, wellness programs, mental health services, and preventive care.

In many cases, the employer pays a part of the insurance premium. The employee pays the rest. This shared cost makes it easier for employees to afford health coverage. It also encourages them to take care of their health.

Eligibility Criteria

Not everyone can enroll in an employer-provided health plan. There are certain eligibility criteria that must be met. Typically, full-time employees are eligible. Part-time employees may also qualify, depending on the company’s policy. In some cases, temporary or contract workers can join the plan.

Eligibility might also depend on the length of employment. For example, new hires may have to wait for a probationary period before joining the plan. This period can range from one to three months.

Family members of employees can often be covered too. This usually includes spouses and children. Sometimes, domestic partners are also eligible. Each plan has its own rules, so it’s important to check the specific details.

Below is a table that summarizes the common eligibility criteria:

| Eligibility Criteria | Details |

|---|---|

| Full-Time Employees | Usually eligible for coverage |

| Part-Time Employees | May be eligible based on company policy |

| Temporary or Contract Workers | Eligibility varies by company |

| Probationary Period | New hires may wait 1-3 months |

| Family Members | Spouses, children, and sometimes domestic partners |

Short-term Health Insurance

Short-term health insurance, also known as temporary health insurance, offers coverage for a limited period. It is designed to fill gaps in coverage during transitions. This type of insurance is not meant for long-term needs but provides essential protection when needed most. Short-term plans often come with lower premiums, making them an affordable option for many.

Temporary Coverage

Short-term health insurance provides temporary coverage during life changes. These plans are ideal when between jobs or waiting for other insurance to start. Short-term policies usually last from one month to a year. They cover unexpected medical expenses like emergency room visits or surgeries. Routine check-ups and preventive care might not be included. It’s crucial to check the specifics of each plan.

When To Consider

Consider short-term health insurance during job changes or recent college graduation. It is also useful when waiting for Medicare or during Open Enrollment periods. If you miss the Open Enrollment deadline, a short-term plan can be a good stopgap. This insurance is also handy when traveling outside your usual coverage area.

Short-term health insurance is not suitable for everyone. Those with pre-existing conditions might not get covered. Families needing comprehensive coverage should look elsewhere. Assess your needs carefully before choosing a plan.

Credit: www.alliancehealth.com

Medicare Plans

Medicare plans provide health insurance for people aged 65 and older. Some younger individuals with disabilities also qualify. Understanding the different types of Medicare plans is essential to choose the right coverage. This guide will help you navigate through the various options available.

Eligibility And Coverage

Eligibility for Medicare is based on age or disability. Most people qualify at age 65. Younger people with certain disabilities or conditions may also be eligible. Coverage includes hospital stays, medical services, and prescription drugs. Each part of Medicare covers different aspects of healthcare.

Types Of Medicare

Medicare is divided into four main parts:

- Medicare Part A: Covers hospital stays, skilled nursing facility care, hospice, and some home health care.

- Medicare Part B: Covers doctor visits, outpatient services, medical supplies, and preventive services.

- Medicare Part C (Medicare Advantage): An alternative to Original Medicare that offers additional benefits. These plans are offered by private companies.

- Medicare Part D: Provides prescription drug coverage. These plans are also offered by private companies.

Each part of Medicare has its own benefits and costs. It’s crucial to understand what each part covers to make an informed decision.

| Medicare Part | Services Covered | Provider |

|---|---|---|

| Part A | Hospital stays, hospice, skilled nursing | Government |

| Part B | Doctor visits, outpatient services | Government |

| Part C | All Part A and B services, extra benefits | Private companies |

| Part D | Prescription drugs | Private companies |

Choosing the right Medicare plan depends on your health needs and budget. Review each part carefully to understand the benefits and costs. This will help you select the best plan for your situation.

Medicaid Plans

Medicaid plans provide health insurance for individuals with low income. These plans help cover medical costs and offer a range of benefits. Medicaid is funded by both the federal and state governments. It’s essential to understand the different aspects of Medicaid plans to make the most of this valuable resource.

State-specific Options

Medicaid plans can vary significantly from state to state. Each state has its own set of rules and benefits. This means that what is covered in one state might not be covered in another.

| State | Specific Benefits | Coverage Limits |

|---|---|---|

| California | Dental, Vision, Mental Health | Varies by income level |

| Texas | Pregnancy, Emergency Services, Prescription Drugs | Varies by income level |

| Florida | Long-Term Care, Family Planning | Varies by income level |

It’s crucial to check your state’s specific Medicaid website. This will give you the most accurate and up-to-date information.

Eligibility Requirements

Eligibility for Medicaid plans is based on several factors. The primary factor is income level. Each state sets its own income limits, and these limits can change.

- Income Level: Must be below a certain threshold.

- Household Size: Larger households may have higher income limits.

- Disability Status: Certain disabilities can qualify you for Medicaid.

- Age: Some programs are designed for children or the elderly.

- Pregnancy: Pregnant women often qualify for Medicaid.

It’s important to apply for Medicaid even if you think you might not qualify. The rules change often, and you might be eligible for benefits you didn’t expect.

In summary, understanding Medicaid plans involves knowing your state’s specific options and eligibility requirements. This can ensure you get the coverage you need.

Choosing The Right Plan

Choosing the right health insurance plan can be challenging. Everyone has unique needs and preferences. Finding a plan that fits your lifestyle is crucial. This section will guide you through the steps.

Assessing Needs

First, assess your healthcare needs. Do you visit doctors often? Do you need regular prescriptions? Are there specific treatments you need? Your answers will guide your plan choice. Families have different needs than singles. Consider any chronic conditions. Think about your budget too. Balancing cost and coverage is key.

Comparing Plans

Next, compare different plans. Look at what each plan covers. Check the list of doctors and hospitals. Are your preferred providers included? Review the cost details. Premiums, deductibles, and co-pays can vary. Understand the terms and conditions. Some plans may offer more benefits. Others may have lower costs. Compare each plan side by side. This helps you see the differences.

Ask questions if needed. Get clear answers before deciding. Choosing the right plan takes time. It’s worth the effort for your health and peace of mind.

Common Health Insurance Terms

Understanding health insurance can be challenging. There are many terms that can confuse you. Here, we explain common health insurance terms. Knowing these will help you choose the right plan.

Premiums And Deductibles

The premium is the amount you pay for your health insurance. You usually pay it monthly. A deductible is the amount you pay for care before your insurance starts to pay. For example, if your deductible is $1,000, you pay the first $1,000 of covered services yourself.

Copayments And Coinsurance

A copayment, or copay, is a fixed amount you pay for a service. For instance, you might pay $20 for a doctor visit. Coinsurance is different. It is a percentage of the cost of a service. After you meet your deductible, you might pay 20% of the cost of a surgery. Your insurance covers the rest.

Credit: www.onsurity.com

Credit: smartfinancial.com

Frequently Asked Questions

What Are The Main Types Of Health Insurance?

The main types of health insurance are employer-sponsored, individual, Medicare, Medicaid, and short-term health insurance. Each type has its own benefits, coverage options, and eligibility requirements.

How Does Employer-sponsored Health Insurance Work?

Employer-sponsored health insurance is provided by your employer as part of your benefits package. It often covers a portion of your medical expenses and may offer additional benefits.

What Is Individual Health Insurance?

Individual health insurance is a policy you purchase for yourself or your family. It provides coverage for medical expenses and can be customized to fit your needs.

Who Is Eligible For Medicare?

Medicare is a federal health insurance program for people aged 65 and older, and some younger individuals with disabilities. Eligibility depends on age and medical condition.

Conclusion

Understanding the types of health insurance is crucial. It helps in making informed decisions. Each option has its benefits. Knowing these can save time and money. Choose the right plan that meets your needs. Consult a professional if unsure. Stay informed and protect your health.

Your future self will thank you.