Life insurance provides financial security for your loved ones after you’re gone. It’s a crucial part of financial planning.

Understanding different types of life insurance can help you make better choices. Each type offers unique benefits, catering to various needs and situations. Some policies are straightforward, while others have complex features. Knowing the differences can save you money and ensure your family’s future is protected.

In this blog, we’ll explore the main types of life insurance. We’ll break down their characteristics and uses. This will help you decide which type suits your needs best. Whether you’re new to life insurance or looking to switch policies, this guide is for you. Let’s dive in and find the right life insurance for you.

Introduction To Life Insurance

Life insurance provides financial security for your loved ones after your death. It ensures that your family can meet their financial needs. Understanding life insurance can help you choose the right policy for you.

Importance Of Life Insurance

Life insurance protects your family from financial hardship. It covers expenses like mortgage payments and daily living costs. Your family can maintain their standard of living even if you are not there.

A life insurance policy can also cover funeral expenses. This can ease the burden on your loved ones during a difficult time. Some policies even build cash value over time.

Having life insurance gives peace of mind. You know your family will be taken care of. This financial protection is crucial for anyone with dependents.

Basic Concepts

Life insurance comes in different types, each with its own features. Term life insurance provides coverage for a specific period. Whole life insurance offers lifetime coverage and accumulates cash value.

Premiums are the payments you make to keep the policy active. Beneficiaries are the people who receive the insurance money after your death. Understanding these terms helps you make informed decisions.

Choosing the right policy depends on your needs and financial goals. Assess your family’s needs and your budget before selecting a policy. This ensures you get the best coverage for your situation.

Credit: www.westernsouthern.com

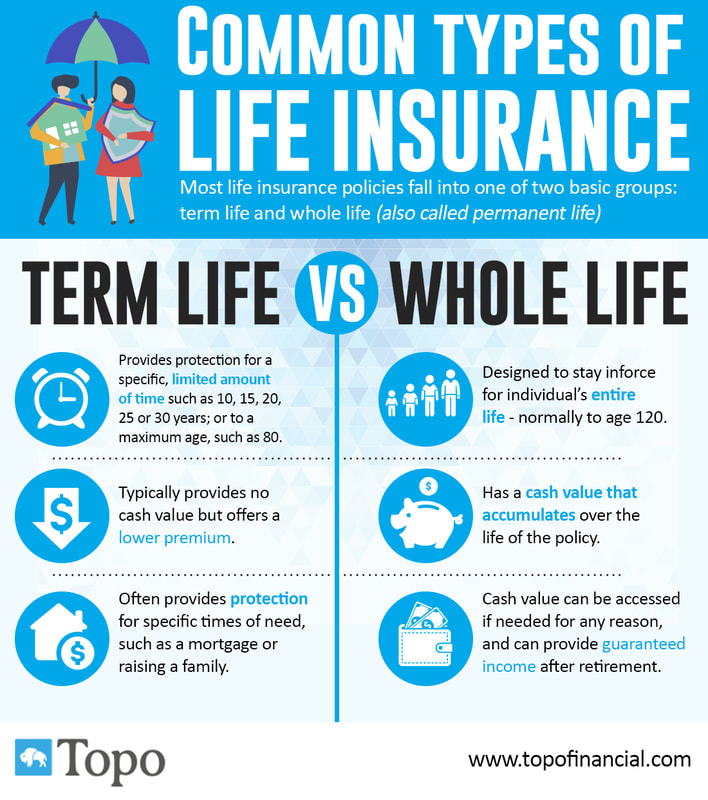

Term Life Insurance

Term Life Insurance is a popular choice for many individuals and families. It provides coverage for a specific period, typically ranging from 10 to 30 years. If the policyholder dies during the term, the beneficiaries receive a death benefit. This type of insurance is generally more affordable than whole life insurance, making it accessible to more people.

Key Features

Term Life Insurance has several key features that make it appealing:

- Fixed Term: Coverage lasts for a predetermined number of years.

- Death Benefit: A lump sum is paid to beneficiaries if the policyholder dies within the term.

- Lower Premiums: Premiums are typically lower compared to whole life insurance.

- No Cash Value: Unlike whole life insurance, term policies do not build cash value.

Pros And Cons

| Pros | Cons |

|---|---|

|

|

Whole Life Insurance

Whole life insurance is a popular type of life insurance. It offers lifelong coverage and has a unique savings component. This type of policy can be beneficial for many reasons. Let’s explore some key features of whole life insurance.

Permanent Coverage

Whole life insurance provides permanent coverage. This means it covers you for your entire life, as long as you pay the premiums. You never need to worry about losing coverage due to age. This offers peace of mind and financial security for your loved ones.

Cash Value Component

One of the unique features of whole life insurance is the cash value component. This is a savings part of your policy that grows over time. A portion of your premium payments goes into this cash value. It earns interest, and you can access it if needed. You can borrow against it or even withdraw some of it. This can be useful in times of need or for future planning.

Credit: www.physiciansidegigs.com

Universal Life Insurance

Universal Life Insurance is a popular choice for those seeking flexibility in their life insurance plan. It offers policyholders the ability to adjust premiums and death benefits to fit their changing needs. This type of insurance also provides investment opportunities, allowing the cash value to grow over time.

Flexible Premiums

One of the key features of Universal Life Insurance is its flexible premiums. Policyholders can choose to pay higher or lower premiums, depending on their financial situation. If you have a good month, you can pay more, increasing the cash value. During tough times, you can pay less, as long as there is enough cash value to cover the insurance costs.

| Situation | Premium Adjustment |

|---|---|

| High Income Month | Pay More |

| Low Income Month | Pay Less |

Investment Opportunities

With Universal Life Insurance, policyholders can benefit from investment opportunities. The cash value portion of the policy can be invested in various accounts. These accounts might include stocks, bonds, or money market funds. This investment potential allows the cash value to grow over time.

- Stock Market Investments

- Bond Investments

- Money Market Funds

The growth of the cash value depends on the performance of these investments. This means that the policyholder can potentially see significant growth in their policy’s cash value.

Variable Life Insurance

Variable Life Insurance is a type of permanent life insurance. It offers both a death benefit and an investment opportunity. This policy allows you to invest the cash value in various accounts. These accounts can include stocks, bonds, and mutual funds. Here’s a closer look at the investment options and risk factors involved.

Investment Options

With Variable Life Insurance, you have several investment options. These options allow you to grow the cash value of your policy. Common investment choices include:

- Stocks

- Bonds

- Mutual Funds

- Money Market Accounts

Each option has its own potential for growth and risk. You can diversify your investments across different accounts. This can help balance risk and return.

| Investment Type | Potential Return | Risk Level |

|---|---|---|

| Stocks | High | High |

| Bonds | Moderate | Moderate |

| Mutual Funds | Varies | Varies |

| Money Market Accounts | Low | Low |

Risk Factors

Variable Life Insurance comes with certain risk factors. The cash value and death benefit can fluctuate. This fluctuation depends on the performance of your investments. Key risks include:

- Market Risk: Investment returns are not guaranteed. The value can go up or down.

- Policy Charges: Fees and charges can reduce the cash value.

- Investment Choices: Poor investment choices can lead to losses.

It’s important to understand these risks before choosing a Variable Life Insurance policy. You must be comfortable with the potential for loss. Always consider your financial goals and risk tolerance.

Final Expense Insurance

Final Expense Insurance is a type of life insurance designed to cover funeral costs and other end-of-life expenses. It provides peace of mind for your loved ones, ensuring they won’t face financial burdens after you pass away.

Coverage For Final Expenses

Final Expense Insurance covers costs like funeral services, burial, cremation, and any related bills. It also helps with medical bills, legal fees, and outstanding debts. This ensures families can focus on grieving, not on financial stress.

Target Audience

Final Expense Insurance is ideal for seniors who want to ease the burden on their families. It’s also suitable for individuals with limited savings or those who want a straightforward plan. This insurance is perfect for people seeking a simple, affordable solution for end-of-life expenses.

Group Life Insurance

Group life insurance is a type of life insurance policy that covers a group of people, usually employees of a company. This insurance provides a safety net for employees’ families in case of an unfortunate event. Group life insurance is often more affordable than individual life insurance policies.

Employer-provided Benefits

Many employers offer group life insurance as part of their benefits package. This insurance is often at no cost to the employee. It provides basic life insurance coverage based on the employee’s salary. For example, an employee might receive coverage equal to one or two times their annual salary. This coverage can help provide financial security to an employee’s family.

Supplemental Options

Employees can often choose to buy additional life insurance coverage. These are called supplemental options. Supplemental options allow employees to increase their coverage beyond the basic amount. This can be important for those with larger financial obligations or dependents. Employees can usually purchase these options through payroll deductions.

Credit: www.topofinancial.com

Choosing The Right Policy

Choosing the right life insurance policy can be challenging. Each type has unique features and benefits. It’s important to understand your needs and compare different policies. This will help you make an informed decision.

Assessing Your Needs

Before picking a policy, assess your needs. Consider your financial goals, family situation, and future plans. Ask yourself:

- How much coverage do I need?

- What can I afford to pay in premiums?

- How long do I need the coverage?

Answering these questions will help you narrow down your options. For example, if you have young children, you may need a policy that offers long-term coverage. If your budget is tight, you might prefer a policy with lower premiums.

Comparing Different Policies

There are several types of life insurance policies. Here’s a brief comparison:

| Policy Type | Features | Best For |

|---|---|---|

| Term Life Insurance | Low premiums, fixed term | Temporary needs, limited budget |

| Whole Life Insurance | Lifetime coverage, cash value | Long-term security, wealth building |

| Universal Life Insurance | Flexible premiums, cash value | Flexible needs, investment opportunity |

| Variable Life Insurance | Investment options, cash value | High-risk tolerance, investment focus |

Compare these policies based on your needs. Term life insurance is ideal for those seeking low premiums and temporary coverage. Whole life insurance offers lifetime coverage and builds cash value. Universal life insurance provides flexible premiums and cash value options. Variable life insurance caters to those with a higher risk tolerance and investment goals.

By assessing your needs and comparing policies, you can find the right life insurance policy. This ensures peace of mind and financial security for your loved ones.

Frequently Asked Questions

What Are The Main Types Of Life Insurance?

The main types of life insurance are term life, whole life, and universal life. Term life insurance offers coverage for a specific period. Whole life provides lifetime coverage and builds cash value. Universal life offers flexible premiums and adjustable coverage.

How Does Term Life Insurance Work?

Term life insurance provides coverage for a specific period, usually 10, 20, or 30 years. If the insured dies within this term, the beneficiaries receive the death benefit. If the term expires, coverage ends without any payout.

What Is Whole Life Insurance?

Whole life insurance offers lifetime coverage and includes a savings component. It builds cash value over time, which you can borrow against. Premiums are generally higher but remain fixed throughout the policy’s life.

Is Universal Life Insurance Flexible?

Yes, universal life insurance is flexible. It allows you to adjust your premiums and death benefits. This flexibility helps you adapt to changing financial situations while maintaining coverage. It also builds cash value, which can be used for loans or withdrawals.

Conclusion

Choosing the right life insurance is crucial for your family’s future. Understand your needs and explore various options. Term life insurance offers coverage for a set period. Whole life insurance provides lifelong protection with cash value. Universal life insurance allows flexible premiums and death benefits.

Each type has unique benefits. Consult a financial advisor to make an informed decision. Protect your loved ones with the best life insurance plan for your situation. Make your choice wisely.